WHAT ARE WE FORGETTING?

Point du Hoc’s reminder for investors

On a cloudy June afternoon in 1984, President Ronald Reagan stood atop the cliffs at Point du Hoc in Normandy, France, to commemorate D-Day. He chose this location because four decades earlier two hundred U.S. Army Rangers had scaled its steep cliffs under direct Nazi fire during the assault.

He spoke to the surviving Rangers who had made the trip across the Atlantic to be there in person, but also to those who couldn’t. More importantly, he honored those who had given their lives that day.

While Reagan certainly wanted to honor the soldiers’ bravery, it wasn’t his sole objective. He also wanted to remind the countless Americans who were starting to forget.

Forget?

Yes, forget.

By the mid-1980s, with World War II nearly forty years in the rearview mirror, two generations of Americans hadn’t experienced a world on the brink. They hadn’t witnessed Adolf Hitler rise to power or fascism spread across multiple continents. They hadn’t seen what happens when a nation convinces itself it can remain isolated from the rest of the world.

Reagan recognized this was a problem. A problem because when people forget the cost of past mistakes, they become far more likely to repeat them.

This is why he used the moment to remind Americans what was at stake—and that while isolationism may feel comforting, its costs inevitably reveal themselves over time.

In his words:

“We in America have learned bitter lessons from two World Wars — that it is better to be here ready to protect the peace than to take blind shelter across the sea, rushing to respond only after freedom is lost. We’ve learned that isolationism never was and never will be an acceptable response to tyrannical governments with an expansionist intent.”

Ultimately, Reagan’s speech was less about World War II than it was about human nature.

The fact is, we have a remarkable ability to forget the lessons of the past unless we experience them ourselves. It is why societies so often repeat mistakes made by prior generations and why we overreact to some risks, while failing to recognize others.

Financial markets and investors are case in point.

When memories of a crisis are fresh, caution dominates. Investors demand safeguards, regulators impose restrictions, and management teams prepare for worst-case scenarios. But as years pass and those scars fade, caution gives way to confidence, confidence leads to optimism, and optimism eventually gives way to excess.

The reality is, when enough time passes, nations, companies, societies, and investors often lose touch with the past. They forget — or perhaps choose to ignore — the reason a decision was made, a safeguard was put in place, or a rule was established.

This principle is closely related to what is known as Chesterton's Fence:

“If a gate is erected across a road, instead of simply removing it because you don’t see the use for it, one should instead consider and determine why it was originally placed there. Then, if its purpose for existing no longer exists, remove it.”

That principle feels particularly relevant today.

Nearly eighteen years removed from the Global Financial Crisis, many Americans have little memory of what a severe recession feels like. A growing number of investors have never experienced a prolonged bear market. Many have never watched a portfolio fall by 50%, seen liquidity evaporate, or witnessed businesses fighting simply to survive.

As a result, investors are currently clamoring for allocations to private companies before they go public, while others chase hot IPOs.

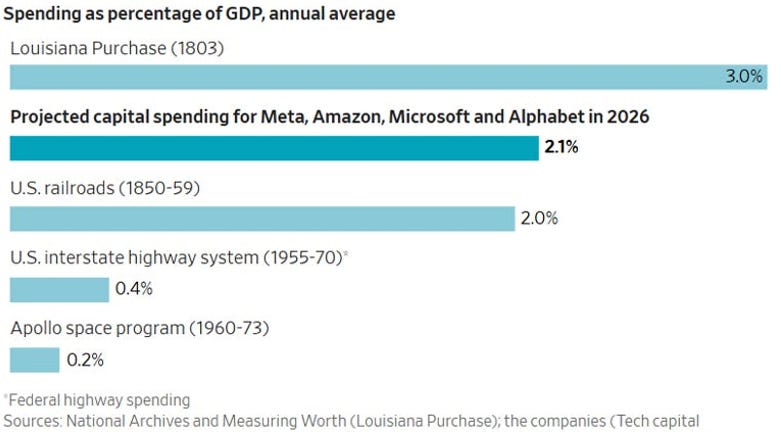

Meanwhile, a select few companies are spending enormous amounts of money in pursuit of artificial intelligence opportunities, with capital commitments that rival some of the most ambitious government-backed programs and speculative booms in modern history.

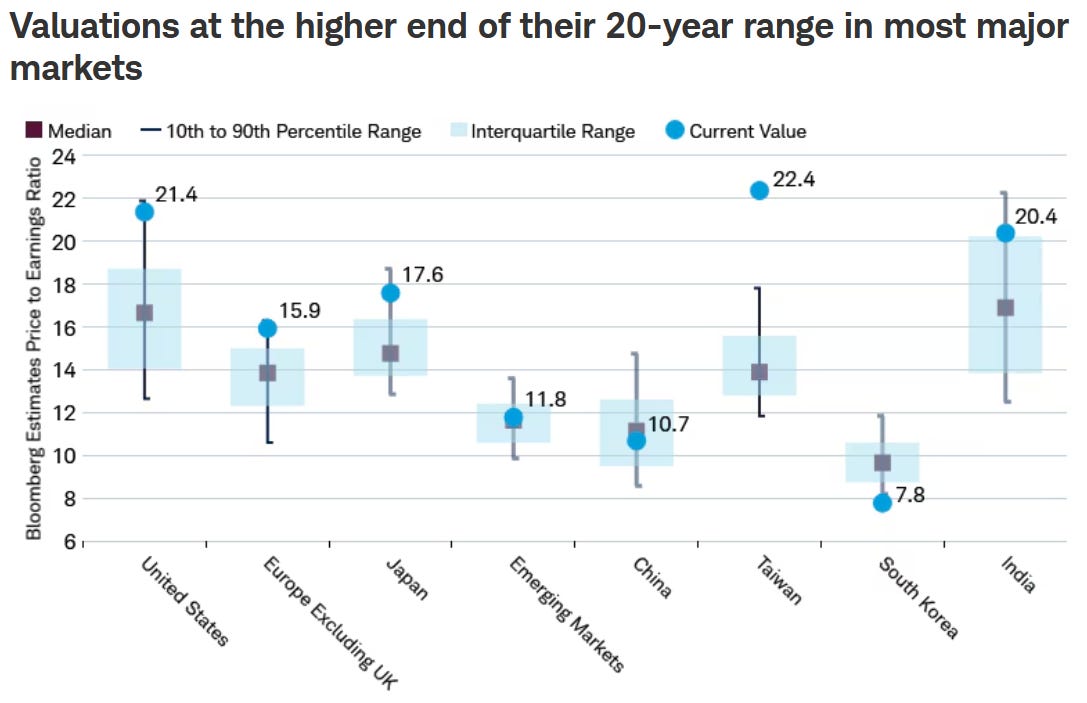

Equity allocations sit near record highs, leaving valuations with little room for error. Animal spirits are fully revved up, and greed is certainly more in vogue than fear.

That said, none of this means disaster is imminent. Nor does it mean today’s opportunities in things like AI are any less real or that the capital spend pursuing it won’t leave a productive wake in its path.

What it does mean, however, is that investors should be careful when dismissing the lessons of the past while considering what lies ahead.

The next crisis will not look like the Global Financial Crisis, just as the Global Financial Crisis did not resemble the dot-com bubble or the inflationary spiral of the 1970s.

However, no matter the backdrop, a similar pattern almost always unfolds:

Fear morphs into confidence. Confidence turns into complacency. Complacency grows into excess. And excess eventually becomes the lesson the next generation has to learn all over again.

That was Reagan’s message at Point du Hoc.

The Rangers climbed those cliffs so future generations would remember what was at stake. Reagan returned forty years later because he feared Americans were beginning to forget.

Given all this, investors should ask themselves the same question:

What are we forgetting?

Possibly that liquidity doesn't matter until it does. Valuations do contract, often violently. Leverage can juice returns on the way up, but cause a lot of pain on the way down. And cycles eventually end. They always do.

Was thinking about this the other day at an allocator panel. One of the allocators said they only invest in managers very early in their lifecycle. Fair enough, the data shows that managers tend to outperform early as they put in the extra hours and have boundless energy. Another allocator told me that they wouldn't invest with a manager with a 10-yr track record for that same reason.

That said, none of these younger managers have been through a 2000-2002, a 2008, or even a 2022. Wondering if in an environment like this it makes sense to lean into experience over ambition.

I recall one wise old manager who declared the main reason emerging managers outperform is they are fearless because they haven't been burned yet. In up markets, fearlessness is rewarded.