SAFER, YET MORE AFRAID THAN EVER

We were close. So Close. Just when Covid-19 appeared to be fading, the largest military conflict since World War II broke out in Eastern Europe leading to devastating consequences for millions of people, spiking commodity prices, weaker equity markets, and geopolitical uncertainty.

Unsurprisingly, countless people have commented how “unbelievable” this series of events has been. But is it? It is really unbelievable? Or, is it actually completely believable? Better yet, is it something we should come to expect by now?

History is riddled with chaos and conflict. Yet, people have an amazing ability to forget this fact. Look no further than former Andreessen Horowitz general partner Balaji Srinivasan’s recent tweet,

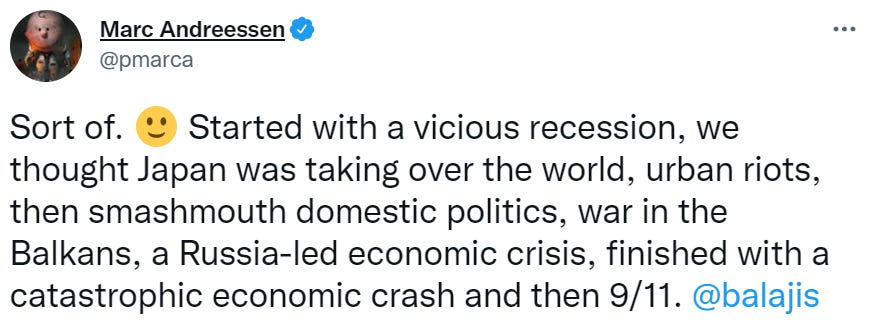

Is Srinivasan right? Were the 1990’s idyllic? Not really, and certainly not in his former boss’s mind. Just look at his response,

Andreessen is right, but this phenomenon doesn’t just apply to the 1990’s.

Every decade has been turbulent. Remember the lines to Billy Joel’s song, “We Didn’t Start the Fire”?

“Harry Truman, Doris Day, Red China, Johnnie Ray; South Pacific, Walter Winchell, Joe DiMaggio; Joe McCarthy, Richard Nixon, Studebaker, television; North Korea, South Korea, Marilyn Monroe; Rosenbergs, H-bomb, Sugar Ray, Panmunjom; Brando, "The King and I", and "The Catcher in the Rye"; Eisenhower, Vaccine, England's got a new queen; Marciano, Liberace, Santayana, goodbye; We didn't start the fire, It was always burning, since the world's been turning. We didn't start the fire. No, we didn't light it, but we tried to fight it.”

And this was just the 1950s.

So why does it so often feel like things are getting worse?

Many reasons, but one that does not get enough attention is tied to how we consume our information these days.

The Filtering Effect

Try something. Click on “MSNBC” and/or “Fox News”. Write down a few of the top stories you see. Seriously. Try it.

Now do the same thing for the New York Times. Now The Dallas Observer. Now the Milwaukee Journal Sentinel. Now the The Annapolis Capital Gazette. And finally The Missoulian. Anything jump out? Trends? Patterns? Takeaways?

As you move away from large media outlets to smaller more local ones, the number of negative headlines drops. The reason? “Fear sells” is the obvious answer, yet there is something else at play. It is called the “filtering effect” and it is having a material impact on society and the markets alike these days.

The filtering effect simply states that whether you are looking at large or small data sets, the averages are very similar, but the extremes are drastically different.

As John Allen Paulos highlights in his book “Innumeracy”, look no further than a river’s water level over varying lengths of time.

“While a river’s average water level over a 25-year period is similar to its water level over any single 1-year period, the most extreme flood during that 25-year period tends to be much more severe than a flood in any given 1-year period.”

This logic applies to countless other things in life.

If you measure 10,000 people or 100 people, the average height will be roughly the same, but you will find a lot more people over 6’6 and under 5’6 among the 10,000 than you will in the 100.

Do the same for SAT scores. The averages will be the same, but there will be a lot more perfect scores in the larger group. The same is true for the weather, sports statistics, and corporate earnings reports.

So why does this matter? Because humans are drawn to extremes and the media (both mainstream and social) knows it.

The Media Food Chain

When major news networks produce a show, they have an endless number of stories to choose from across the world. In essence, every day these networks get to look for extreme floods over a 25-year period.

Now think about the New York Times. It covers the world as well, but also must dedicate a portion of its pages to local New York Tri-State stories. Think of their universe as a river over a 20-year period.

The mid-markets (Dallas and Milwaukee) report much less national and international news, so their universe of stories equates to rivers over 10 to 15-years, while the smallest markets (Annapolis and Missoula) are almost exclusively focused on local news and therefore rivers over 5 to 10-years.

In short, the smaller the market, the fewer extremes to choose from.

So, why is this an issue for people and investors alike? Because since the advent of the 24/7 news cycle and the rise of the internet two decades ago, people have been increasingly consuming more extreme news. Not because the news has gotten more extreme, but rather because people are paying more attention to sources covering larger data sets.

Over the past two decades, weekday newspaper circulation has fallen from roughly 60 million households to less than 26 million, which has caused the number of newspapers in circulation to drop by more than 25% (Statista). At the same time, cable news viewership has risen materially, people like Rachel Maddow and Sean Hannity get paid tens-of-millions of dollars each year, and Twitter “blue checks” have countless followers.

A New Reality?

So given this trend is highly unlikely to reverse, what’s one to do?

While people are becoming increasingly pessimistic, Hans Rosling makes the case in his wonderful book, Factfulness, that if you maintain a “fact-based worldview”, you should feel precisely the opposite way. He writes,

“Think about the world. War, violence, natural disasters, man-made disasters, corruption. Things are bad, and it feels like they are getting worse, right? The rich are getting richer and the poor are getting poorer; and the number of poor just keeps increasing; and we will soon run out of resources unless we do something drastic. At least that’s the picture that most Westerners see in the media and carry around in their heads. I call it the overdramatic worldview. It’s stressful and misleading. Yet, Step-by-step, year-by-year, the world is improving. Not on every single measure every single year, but as a rule. Though the world faces huge challenges, we have made tremendous progress.”

How is the world getting better? Examples include:

Democracy: While the number of autocracies has fallen by close to 90% since 1960 the number of democracies has more than doubled.

Economic: Global income inequality has fallen materially over the past fifty years, while the proportion of the global population living in extreme poverty has halved in the last two decades. Technological advances have been material, GDP per capita in the U.S. has nearly doubled, and interest rates have been at historically low levels (albeit rising recently). For equity investors, the S&P 500 is up close to 500% since the turn of the century, international developed markets are up 240%, and emerging markets +400%.

Violent Crime: Despite the recent pickup, violent crimes have fallen by 50% since 1989 from 800 per 100,000 people per year to less than 400.

Health: Life expectancy is now well into the 80s in the developed world, advances in biotechnology are creating treatments that were once considered unimaginable, some believe we could even be on the verge of curing once debilitating diseases like Cystic Fibrosis, AIDs, and even some cancers.

As Altimeter’s Brad Gerstner said on a recent podcast, there is not enough attention given to the fact that “We live in the most peaceful, notwithstanding Ukraine, most prosperous, and healthiest time in humanity’s history.”

So why don’t we realize and appreciate these sorts of things? Rosling argues it’s because,

“The media and activists rely on drama to grab your attention. Remember that negative stories are more dramatic than neutral or positive ones. Remember how simple it is to construct a story of crisis from a temporary dip pulled out of its context of a long-term improvement. Remember that we live in a connected and transparent world where reporting about suffering is better than it has ever been before. And thanks to increasing press freedom and improving technology, we hear more, about more disasters, than ever before.”

The Impact on Markets

Markets are made up of people. People are emotional. Therefore, markets reflect that emotion. Today, the filtering effect is making people more emotional, which is creating a number of knock-on effects for investors and markets.

Impulsive Decision Making

In short, investors are reacting to news more quickly and impulsively than ever. As Daniel Kahneman highlights in “Thinking Fast and Slow”, this is a result of the “fast, instinctive, and emotional side” of investors’ brains gaining strength over the “slower, deliberate, and logical side”. The result is more reactionary investor behavior, a “sell-first, ask questions later” mentality, and a more volatile market.

Worse Forecasts Than Ever

When people rely more heavily on the emotional side of their brains, their predictive ability falters. Yet, in spite of this fact, people are making bolder proclamations and projections than ever.

Look no further than the belief that Covid-19 was going to cause a Great Depression, a collapse in the equity markets, and lead to a world where handshakes would be permanently replaced by that nonsensical elbow bump.

Or, remember when the U.S. killed the Iranian general, Qasem Soleimani, back in January of 2020 and how this was going to lead to another world war?

How about the forecasts that we had reached “Peak Oil Demand” and that prices would be low forever? Only to be followed by the realization that we may be massively undersupplied with oil and would send prices to $200/barrel?

Or, how about those dire predictions that Brexit was going to lead to the end for Europe, the U.K., or both?

The fact is, the world is always facing challenges and sadly, tragedies. The trouble is that when people make forecasts based on snap judgements in the midst of extreme events, they forget that society is highly incentivized to solve these problems. The result is that these forecasts are almost always wrong. My guess for today’s poster child? The commodity markets.

Pricing Risk

In the real world, home alarm sales in safe suburban neighborhoods have risen materially despite no material rise in crime rates. Why? Could it be because people are sitting at home in front of the nightly news, Twitter, and their Facebook feeds watching CVS’ and Walgreen’s getting ransacked in cities thousands of miles away and thinking to themselves, “My house could be next?” This is irrational behavior, but understandable given the filtering effect.

Investors are no different. Paying too much attention to extreme events often leads to a temptation to pay exuberant sums for tail risk hedges to protect against extremely low probability events, invest in complex investments to mute volatility, sell underperforming assets at precisely the wrong time, and restrict the ability to invest in others.

What Should Investors Do?

Gauging sentiment, assessing probabilities, and pricing risk are three of the most important things that an investor does. The trouble is investors are as vulnerable to the filtering effect as anyone.

Don’t get me wrong. I get sucked into these pitfalls just as much as anyone else. I can’t help myself. I visit the major websites, spend time on Twitter, and watch the evening news. I wish I could tell you that I do what Warren Buffet does and sit alone reading books and reports all day, or go on long walks in the woods for hours to think, but the reality is this just isn’t practical. So, what I do is simply view every headline with a skeptical eye, spend a little more time reading the local metro section of the newspaper and a little less time watching Maddow and Hannity, and find some people on Twitter that I know are more rational than most.

It’s not perfect, but it's better than the alternative.