BENEATH THE SURFACE

Imagine a duck gliding effortlessly across a pond, appearing still, unbothered, and in control of its direction. Yet, out of sight beneath the water, an entirely different story is unfolding: churning its feet, expending energy, and constantly adjusting itself just to stay afloat.

While this imagery is most often used to highlight how many people move through life (i.e., their lives appearing to be smooth and polished on the surface, but much more going on below it), the same can be said for the markets. This year in particular.

So far in 2026, we have witnessed an attack on Iran, oil prices hitting $100, mortgage rates spiking, hiring stagnating, AI threatening to make software obsolete, and the “Mag 7” collectively down roughly 17%. Yet, the S&P 500 is down just 7% year-to-date through the end of last week. Viewed through this lens, the duck has remained relatively stable. However, if you look below the surface you will see a much different picture.

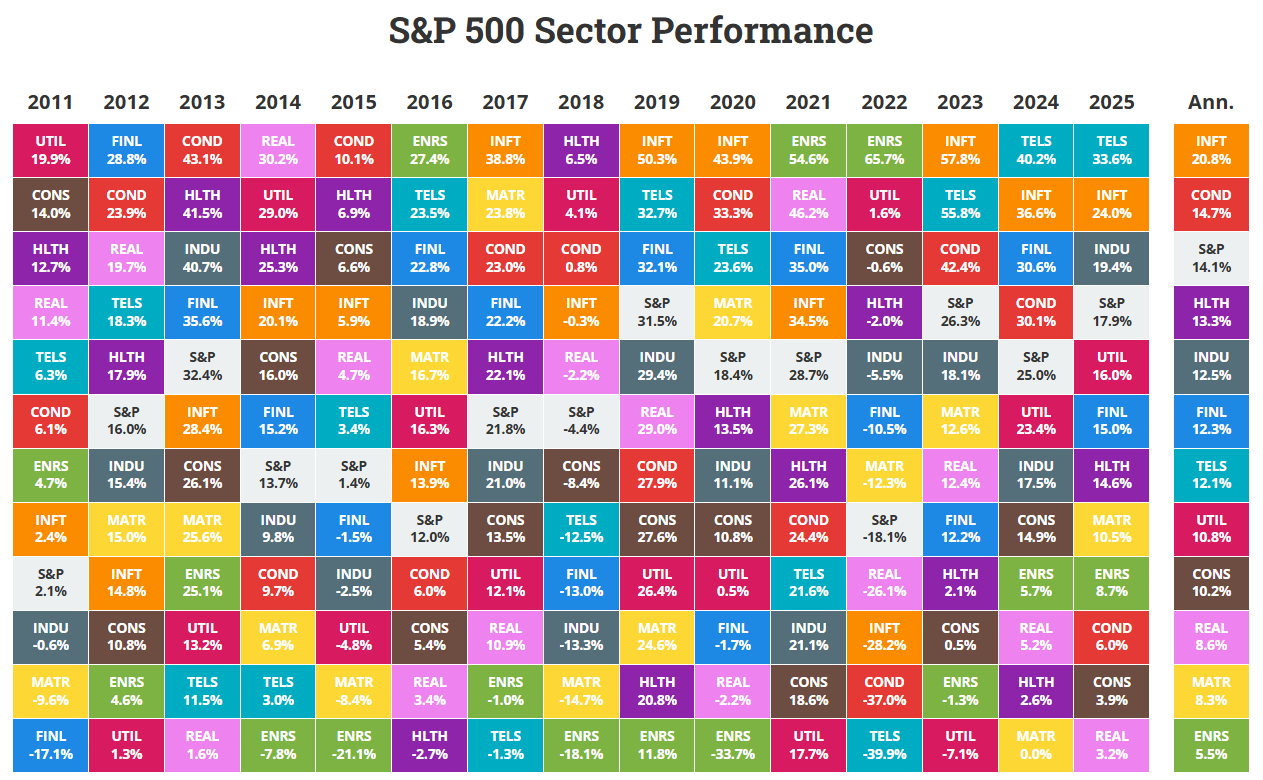

In this case, when I say “below the surface,” I am referring to the eleven respective sectors that make up the market.

Now, before I go any further, take a minute to think about how you would picture it.

With the market down a few percent, how would you expect the underlying sectors to have performed?

More specifically, how far apart would you expect the best and worst performing sectors to be?

10%? (i.e., something like the best sector down 5% and the worst being down 15%?)

15%?

20%?

Something else?

Seriously, take a minute.

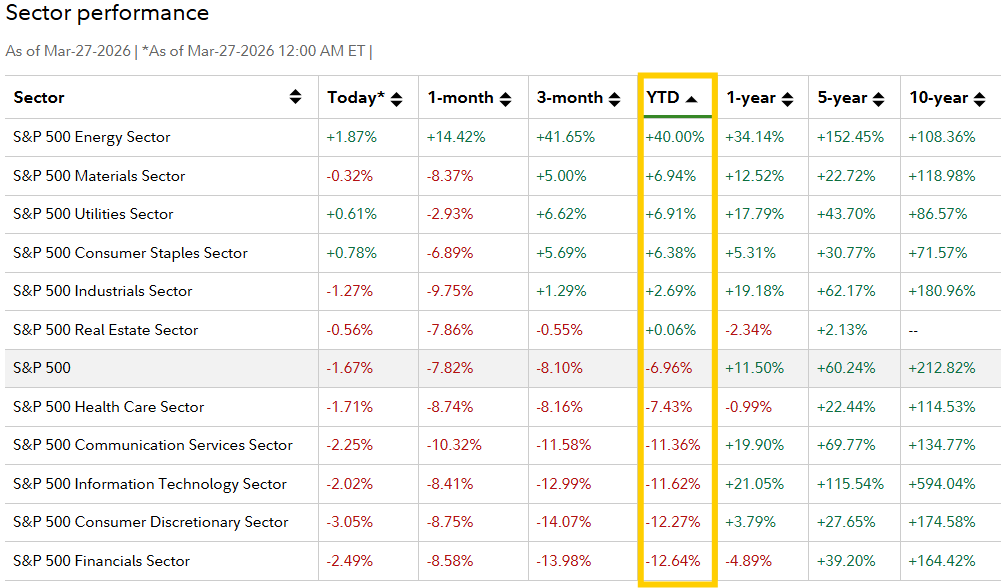

What if I told you that the difference between the best and worst performing sectors through the end of March is more than 50%???

You heard that right…given the energy sector is up 40%, while the four largest sectors — technology, financial, consumer discretionary, and communication services — are each down roughly 12%, the gap is extremely wide.

Sounds unprecedented, right?

Depends on how you look at it. While a 50% gap through the first three months of the year is a lot, just three years ago the difference between the best and the worst sector was over 100% (+65% for energy versus -40% for communication services).

So, why is this important?

In part because of how the market is structured.

In short, because the S&P 500 is “market cap weighted” its larger sectors typically carry more weight. Said another way, since technology represents more than 30% of the index, the fact that it is down close to 12% has a larger impact than energy does at less than 5% of the market with a +40% return.

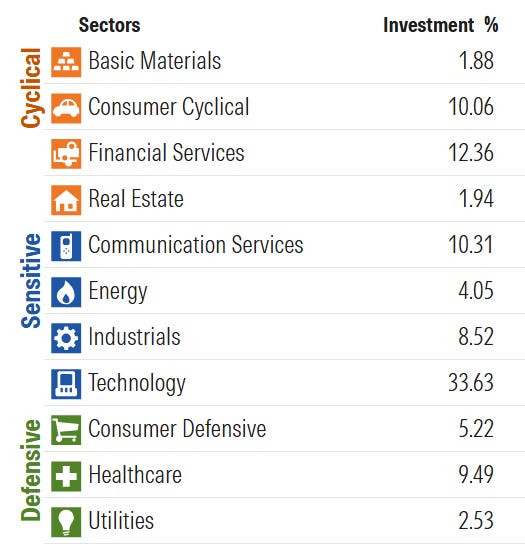

The other thing to consider is that when a sector has outperformed as significantly and for as long as technology has (up close to 600% over the past decade and +900% over the past fifteen years), portfolios tend to become very overweight that sector. This is true because of portfolios’ exposure to the overall market (e.g., passive exposure to the S&P 500), but also when they are invested in things like private assets because the majority of venture, growth equity, and even buyouts and private credit investments are significantly allocated to the technology sector.

Lastly, as it relates specifically to energy, most portfolios have had minimal energy exposure for years now (in part due to its underperformance prior to 2020, but also the ESG movement). As a result, many investors have not benefitted from the sector being up 40% year-to-date or more than 150% over the past five years.

This also means most portfolios haven’t benefitted from the diversification energy provides, especially versus the technology sector.

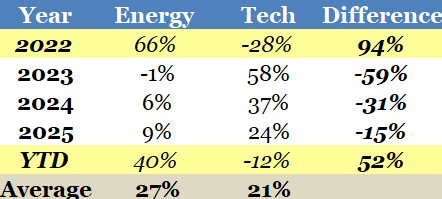

Just look at the past 4+ years. When energy has been up, tech has been down, and vice versa.

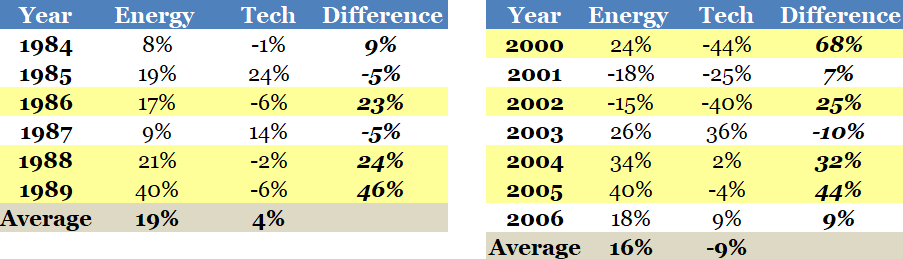

But this stretch is far from the only example. Just look at the mid-1980s or early-2000s:

Think about this for a minute.

If a hedge fund presented this track record to you — one that has outperformed technology by an average of 37% in years when tech has finished a year in negative territory — wouldn’t you beg them to take your money?

Of course you would…and you’d gladly pay “2 and 20” for the privilege (2% annual fee + 20% of the profits). Yet, any investor can obtain this exposure for a few basis points (0.8%) through your basic energy ETF (e.g., XLE).

Knowing this, what does this mean for investors today?

First, from a purely investment standpoint, every portfolio should have an allocation to energy. Given how sizeable tech allocations have become in recent years, this is even more so the case today due to energy’s diversification benefits, but also because even after its recent strong performance, it is still one of the worst performing sectors over the past decade (+108% vs. +594% for tech and +212% for the S&P 500).

Second, it is just more evidence that when a part of the market becomes unloved, disregarded, or even disdained, it is often an indication that it warrants more capital, not less. Not only could it be a “coiled spring,” it can also provide a good counterbalance to a sector that has produced unusually strong and sustained performance.

The reality is that over the past fifteen years, technology has compounded at close to 18% annually, which is ~4% above its historic average. Meanwhile, despite its recent strength, energy has compounded at just 7%, which is close to 3% below its historic average. Yet, investors are still overallocated to the former and under allocated to the latter.

My suggestion?

The surface rarely tells the full story. The real opportunities are found beneath it.

Disclosure: Past performance is not indicative of future results. This material is provided for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Opinions expressed are subject to change without notice and should not be relied upon as the basis for any investment decision.