BE LIKE MIKE...and Paul

In the early 1990s, Michael Jordan was the most popular and recognizable athlete in the world. From the suburbs of Washington D.C. and Dallas, to the inner cities of Chicago and Los Angeles, to the countryside of Indiana and Oklahoma, kids across the country were imitating Jordan’s trademark fadeaway jump shot or “Air Jordan” dunk. I know because I was one of those kids.

Gatorade saw this and capitalized on it with their “Be Like Mike” advertising campaign, which aired for the first time on August 8th, 1991.

If you were born anytime in the 1980s or earlier, you know the tune.

“Sometimes I dream, that he is me. You've got to see that's how I dream to be. I dream I move, I dream I groove. Like Mike, if I could be like Mike. Like Mike, if I could be like Mike.”

Take a minute and watch it here.

For many, it will remind you of your childhood. For others, it will remind you of your kids’ childhoods. For the rest of you, it will provide a glimpse of what life was like before social media monopolized our attention and ad dollars.

Back then, every kid simply wanted to “Be Like Mike.”

It is hard to believe, but Jordan’s popularity persists to this day. Look no further than the fact that Nike’s Jordan brand surpassed an astonishing $5 billion in 2022 despite him retiring more than two decades ago.

Now, in what might be the first time this parallel has ever been drawn, what Jordan has been to every aspiring young athlete, Paul Volcker has been to every aspiring central banker.

My sense is this includes Jerome Powell.

Said another way, all central bankers want to “Be Like Paul.”

More importantly, none want to “Be Like Arthur”.

Who?

Exactly.

While many people have heard of Paul Volcker given he is responsible for defeating the inflation that ravaged the U.S. economy in the 1970s, few recognize the name of the man who enabled it to persist and spread.

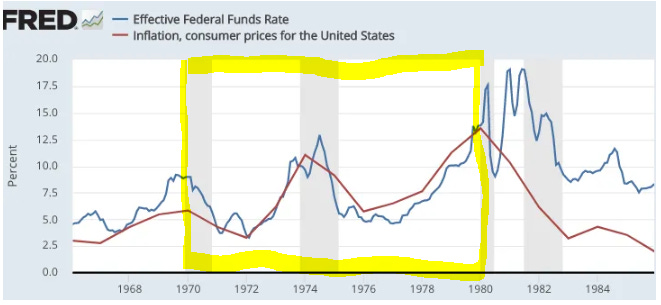

When Arthur Burns was appointed the 10th Chairman of the Federal Reserve in 1970, inflation was rising as a result of the massive government spending associated with Lyndon Johnson’s “Great Society”, the Vietnam War, and higher oil prices that resulted from OPEC’s increased control of the market.

Burns’ task was clear — get it under control.

Things started out promising as Burns increased short-term rates above inflation (creating positive “real rates”). The problem was he did not have the fortitude to keep them high enough for long enough. Instead, each time inflation fell in response to lower economic growth and higher unemployment (see the 1970 and 1974 recessions highlighted in grey in the chart below), Burns balked under political pressure and cut rates (see the fact that the blue line never stayed above the red line for any meaningful period of time during the 70s).

As a result, like someone on a diet who goes back to their poor eating habits after hitting their target weight only to pack the pounds right back on, any retreat in inflation proved to be temporary since the Fed never kept real rates positive for long enough.

This damaged the Fed’s credibility, which resulted in the market losing faith in its wherewithal and ability to fight inflation.

The result?

As William Sibler highlights in his book, “Volcker,” inflation changed people’s behavior.

“An inflationary virus had wormed its way into people’s brains and altered their consciousness. Tessie Rogers, a divorced mother of two from Atlanta, said, ‘I just bought a house and the biggest reason I did it was because I was afraid that if I didn’t do it now, tomorrow might be too late.’ Terry Grantham, a college student and painter’s helper from Lubbock, Texas, lamented that, ‘Every day that goes by it seems like the money I have doesn’t buy as much. I was raised a steak and potatoes boy but now it ain’t that way anymore. It’s hamburger and bologna.’ And Kathy Neuhas, whose husband was an East Hampton police officer, confessed to borrowing money to go to an amusement park for fear that if they didn’t do it now, they never would be able to afford it.”

This remained the case until Paul Volcker arrived on the scene.

In 1980, Volcker doubled the Fed Funds rate from ~10% to 20% (for a point of reference, Powell has raised it from ~0% to 5.5% in ~18 months). Most importantly, unlike Burns, Volcker kept real rates in positive territory for the entire duration of his chairmanship in order to stamp out inflation (see yellow box in chart).

Volcker eventually accomplished his mission, as evidenced by the fact that inflation fell from an astonishing 14% in 1980 to 6% in 1982 and under 2% by 1986. However, this did not come without economic pain as unemployment peaked at nearly 12%. Yet, this pain would prove to be “just the medicine” the economy needed and helped usher in one of the strongest periods of economic growth in U.S. history.

So, why do I bring this up?

Why do I draw this bizarre analogy between Jordan and Volcker?

Because if I am correct in the belief that Jerome Powell ascribes to the “Be Like Paul” mantra, the only people who should expect the Fed to meaningfully cut rates anytime soon are the same people who thought Sam Bowie was the better #2 pick than Michael Jordan in the 1984 NBA Draft.

Who?

Exactly.

Powell told us as much last week when he said that inflation was still too high and warned that more interest rate increases were still possible if economic growth and/or employment data remained stronger than expected.

Additionally, more than a year ago Powell highlighted how the inflationary 1970s guides his policy decisions when he said,

“History cautions us strongly against prematurely loosening policy (specifically as it relates to the period between the Arab oil crisis in 1974 and Iranian oil crisis in 1980). The successful Volcker disinflation in the early 1980s followed multiple failed attempts to lower inflation over the previous 15 years.”

Today, with energy prices rising, a serious conflict in the Middle East brewing, tensions with Russia and China at a fever pitch, government debt at extreme levels, workers striking more frequently, and inflation still at stubbornly high levels, the inflationary era from close to five decades ago has to be as top of mind as ever.

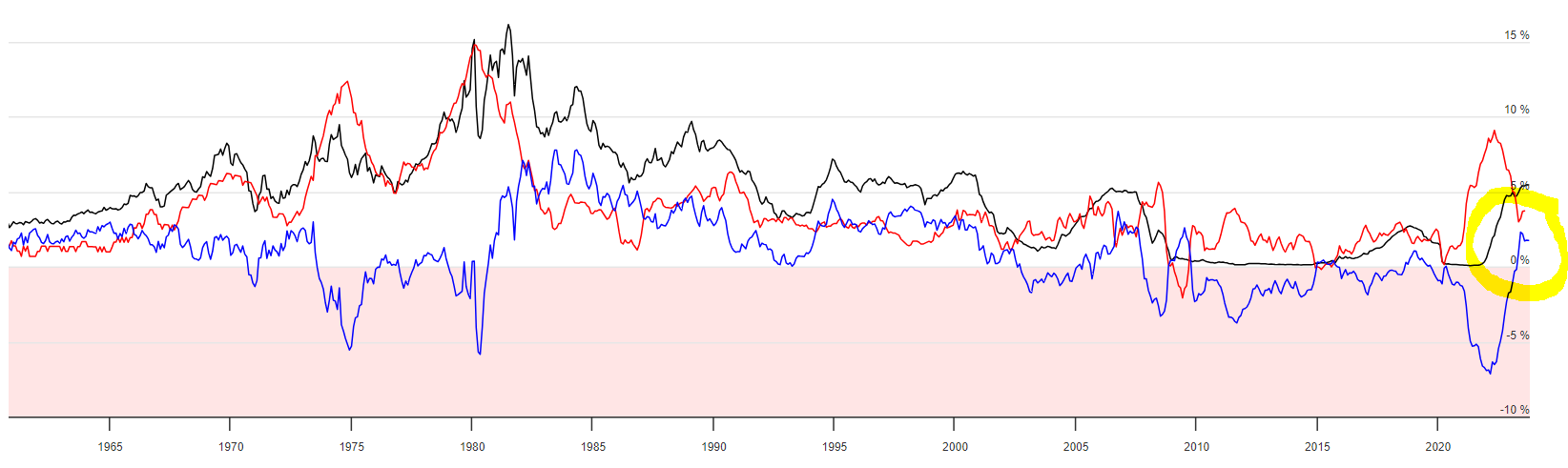

If so, while many people are watching and talking about nominal rates and whether the Fed is going to cut or not, I would be focusing more closely on real rates because while Volcker remained committed to keeping them positive for years, Burns did not.

Considering real rates only turned positive recently (as seen by the blue line below moving above the 0% threshold), I suspect we have a pretty long road ahead of us.