A BLOODBATH IN THE CLOUD

It’s been a bloodbath in the cloud given the software index has fallen close to 30% since October. The story is even worse for some of the more notable companies in the iShares software ETF (“IGV”):

Figma -55%

Hubspot -50%

TradeDesk -45%

ServiceNow -45%

Oracle -45%

Atlassian -40%

Workday -35%

At this point we all know why — practically overnight, investors became convinced that artificial intelligence is a superior technology that could replace software altogether.

So, when might this occur?

No one knows, but it actually doesn’t really matter because so long as investors believe it is only a matter of “when” and not “if”, the selling pressure will continue.

While I certainly can’t tell you when (or frankly if) AI will upend software, I can tell you this — there is a pattern to keep an eye out for. A pattern from the past that could provide clues as to how this current dynamic might unfold.

In the early 1980s, mutual funds ruled the investing world, while private equity firms, quant-driven outfits, and hedge funds were just a blip barely on people’s radar. For decades, stock market investing had been out of reach for most everyday Americans, but mutual funds changed that by flinging the doors (really, the floodgates) wide open to equities. Assets poured in, revenues exploded higher, and powerhouses like Fidelity, PIMCO, and T. Rowe Price became dominant players. Their top portfolio managers turned into household names in an era when picking stocks was suddenly accessible to the masses.

When the 1990s arrived, these funds were riding high with no end in sight. But as history has shown time and time again, the problem with outsized success and profits is that it inevitably leads to more competition. More innovation. More alternatives. As Tony Fadell, the Apple engineer responsible for the iPod, said in his book Build,

“Competition is both direct and indirect. Someone is always watching, trying to exploit any crack in a successful competitor.”

This was certainly the case for actively managed mutual funds, and it came from all directions.

Blackrock, State Street, and Vanguard took them on directly with passive alternatives. Meanwhile, Blackstone, KKR, and Apollo flanked them with private equity. More recently, like Magua and the other Huron warriors ambushing the British soldiers in The Last of the Mohicans, Ken Griffin’s Citadel and the other pod shops have been dealing some of the newest blows.

So, what has happened to mutual fund companies as a result of this onslaught in competition?

Some, like Wellington and Fidelity, who adapted to the times by modernizing their investment platforms continued to succeed (their private ownership structures helped as well). However, many of those who didn’t struggled. Others went out of business, some were acquired, while the rest are still around but grasping for relevance.

I would expect the same story to unfold in software. Some companies will adapt and be fine. A few might even thrive and actually take market share as a result of others’ struggles, and even leverage AI. On the flip side, those that don’t adapt likely will not make it. Meanwhile, many will find themselves in the “messy middle”. These are the companies that want to adapt, but can’t make enough changes to avoid slipping from dynamic market leaders to more commoditized infrastructure providers.

The mutual fund comparison is far from the only one. You’ve likely heard endlessly about railroads in the 1800s, but it’s also happened in sectors such as national defense following the “last supper” in the early 1990s, tobacco companies following the onslaught of class-action lawsuits, and most recently in the office market following the work-from-home phenomenon.

What makes now a little different is just how quickly things are happening. New entrants emerge out of thin air. News and speculation travel instantaneously. Markets price things in even faster.

And herein lies the dilemma for investors.

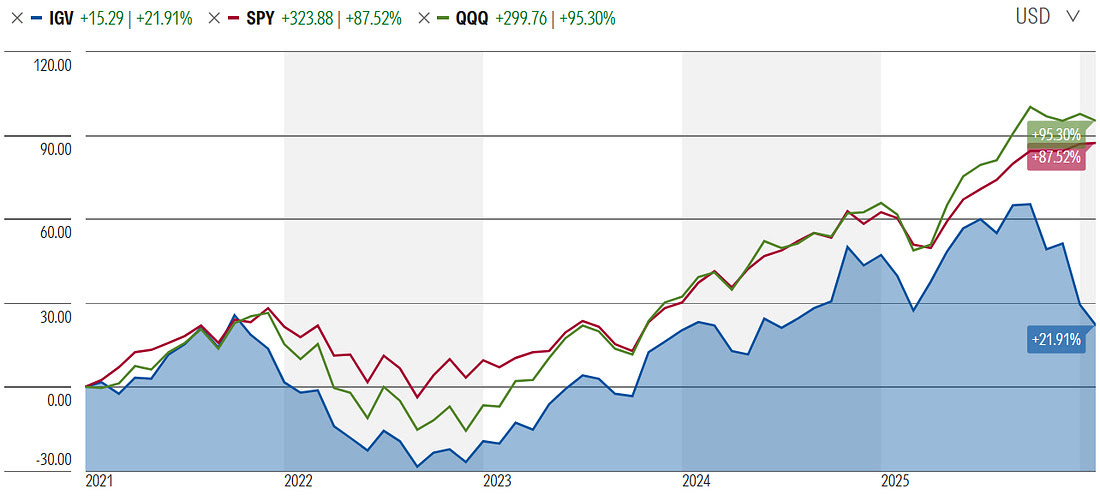

Not only have public software stocks been volatile, they’ve also lagged both the S&P 500 (“SPY”) and NASDAQ (“QQQ”) for more than five years in the face of slowing growth, contracting multiples, and employees unloading their stock options.

At the same time, private market investors are asking themselves whether it’s worth it to lock up their money for 10–15 years in technology businesses whose durability is now under intense scrutiny. Who operate in an environment that can be upended in a matter of months. Whose moats can disappear seemingly out of thin air.

So, what is an investor to do?

One way, as a recent Substack titled “Patient Capital Will Eat the World,” is to lengthen your time horizon. Abandon the quarterly performance derby and the traditional private fund model. Instead, favor structures that eschew finite time periods and fund lives, choosing instead to hold assets forever. A permanent holding if you will. One that doesn’t need an exit and instead focuses on the promise of cash flows that will make a terminal value irrelevant. Letting the power law work its magic.

The trouble is that this path isn’t for everyone as it requires enduring a lot of uncertainty for a long period of time.

If so, is there a different path? One with a closer horizon?

Sure. Look to different parts of the market. Or as Josh Brown, aka “The Reformed Broker,” said in a recent post,

“I’m using the backronym H.A.L.O. to describe the types of stocks that I expect to serve as a winning haven from this year’s feverish pitch of disruption fear. HALO stands for ‘Heavy Assets, Low Obsolescence.’ These are undisruptable companies from an AI standpoint. There’s nothing Sundar Pichai and Sam Altman can take from them. HALO stocks are immune to Claude Code. Anytime people are freaking out about Claude Code and ripping capital out of the shares of its perceived gallery of victims, these are the types of stocks that are being bought instead.”

Many investors think that these companies are boring, but as I said in a past post, “Boring Can Be Beautiful.” They sell things like fasteners, refine petroleum, supply replacement auto parts, and even lease office space. Certainly not exciting stuff, but that is precisely why they don’t invite an onslaught of competition the way software has in recent years, or mutual funds did forty years ago. This means they’re relatively “AI immune”. If anything, these companies might even be able to benefit from AI without the risk of being displaced by it.

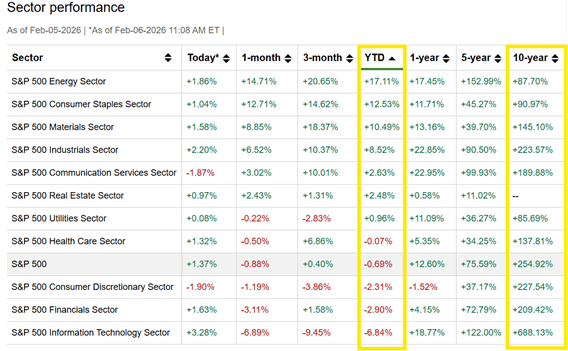

I could be wrong. This might just be one of the endless number of head fakes we’ve witnessed in the past decade. Tech and software might bounce here off the lows, and we could be off to the races again. Yet, for all you value investors out there, it is worth noting that the best performing sectors so far this year are largely the worst performing ones over the past decade. They’re also the ones with the largest amount of “hard assets” and collateral.

Boring? Maybe.

Beautiful? That’s in the eye of the equity holder.